Nokia Corporation Interim Report for Q3 2024

Nokia Corporation Interim Report for Q3 2024

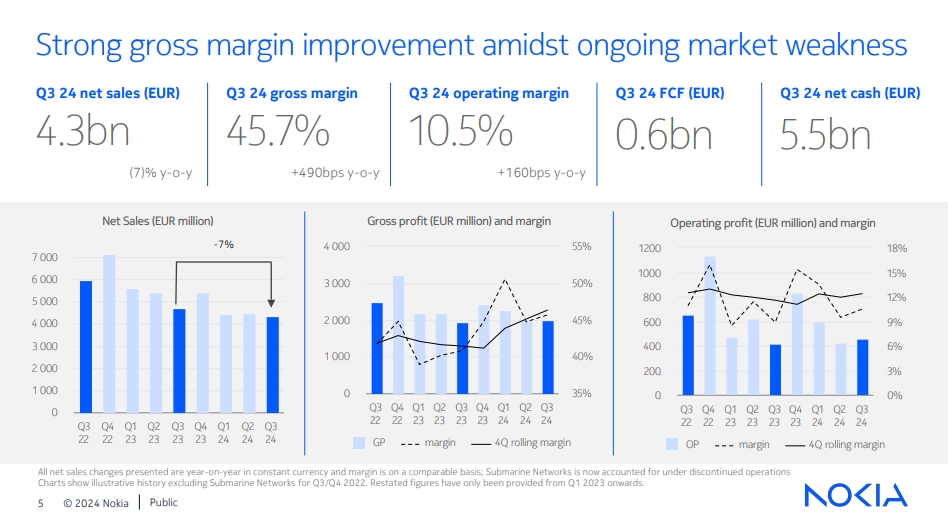

Strong gross margin improvement amidst ongoing market weakness

Q3 net sales declined 7% y-o-y in constant currency (-8% reported) as growth in Network Infrastructure and Nokia Technologies was offset by decline in Mobile Networks primarily in India and a divestment in Cloud and Network Services.

Order intake remained strong in Network Infrastructure, while the sales recovery continues to be slower than expected.

Comparable gross margin in Q3 increased by 490bps y-o-y to 45.7% (reported increased 500bps to 45.2%), with improvements across business groups, particularly in Mobile Networks.

Q3 comparable operating margin increased 160bps y-o-y to 10.5% (reported up 70bps to 5.7%), mainly due to higher gross margin, continued cost control and a benefit from the reversal of loss allowances for certain trade receivables.

Q3 comparable diluted EPS for the period of EUR 0.06; reported diluted EPS for the period of EUR 0.03.

Q3 free cash flow of EUR 0.6 billion, net cash balance EUR 5.5 billion.

Continued to make significant progress with cost savings program, EUR 500 million run-rate of gross savings actioned.

Nokia's full year 2024 outlook is unchanged. Nokia currently expects comparable operating profit of between EUR 2.3 billion and 2.9 billion and free cash flow conversion from comparable operating profit of between 30% and 60%.

This is a summary of the Nokia Corporation Interim Report for Q3 2024 published today. Nokia only publishes a summary of its financial reports in stock exchange releases. The summary focuses on Nokia Group's financial information as well as on Nokia's outlook. The detailed, segment-level discussion will be available in the complete financial report hosted at www.nokia.com/financials. A video interview summarizing the key points of our Q3 results will also be published on the website. Investors should not solely rely on summaries of Nokia's financial reports and should also review the complete reports with tables.

PEKKA LUNDMARK, PRESIDENT AND CEO, ON Q3 2024 RESULTS

As I reflect on our performance in the third quarter, I am optimistic we are now turning the corner in many parts of our business, even if some continue to experience market weakness. Among the key highlights was a return to net sales growth in Network Infrastructure with Fixed Networks growing 9% in constant currency and IP Networks growing 6%. Order intake in Network Infrastructure continued to be robust with strong year-on-year growth and a growing order backlog. Additionally, we delivered a significant improvement in our gross margin at the group level and cash generation remained strong with EUR 621 million free cash flow in the quarter.

There are reasons for optimism across our portfolio. We expect a significant acceleration in growth in Q4 in Network Infrastructure and see a number of structural demand trends supporting our future growth. In Mobile Networks, although market dynamics are more challenging, we have secured several important deals in the quarter, remain confident in our competitive position and are improving our gross margin. In Cloud and Network Services we are seeing excellent momentum in 5G Core along with strong progress in network automation, cloudification and enabling network APIs. Nokia Technologies continues to benefit from greater stability following the conclusion of its smart-phone renewal cycle and is making good progress expanding into the new growth areas.

Across Nokia we are investing to create new growth opportunities outside of our traditional communications service provider market. We see a significant opportunity to expand our presence in the data center market and are investing to broaden our product portfolio in IP Networks to better address this. Our pending acquisition of Infinera will also bolster our Optical Networks exposure to this market and accelerate our growth opportunities. Additionally, we see a compelling new long-term opportunity in bringing 5G technology to the defense market and we continue to invest in private wireless networks where we are the clear market leader.

Regarding our financial performance in Q3, our net sales declined by 7% in the quarter in constant currency. Three quarters of the decline was driven by India due to a strong year-ago quarter. Importantly we delivered a significant improvement in comparable gross margin which expanded 490 basis points from the year-ago period to reach 45.7%. This was driven by a combination of improved product mix, regional mix and actions to reduce product cost. Despite continued intense competition, we remain disciplined on price while still winning deals as we remain focused on improving the profitability of our business. We also progressed our cost reduction efforts contributing to a solid improvement of 160 basis points in our comparable operating margin on a year-on-year basis.

Regarding full year 2024, our comparable operating profit outlook remains EUR 2.3 to 2.9 billion and we are currently tracking within the bottom-half of the range. The net sales recovery is happening slower than we expected previously, however, this is being partially offset by an improving gross margin and quick action on cost. We expect to be at the high end of our free cash flow target of 30% to 60% conversion from comparable operating profit.