Nokia Corporation Report for Q2 and Half Year 2024

Full year outlook reiterated in challenging environment

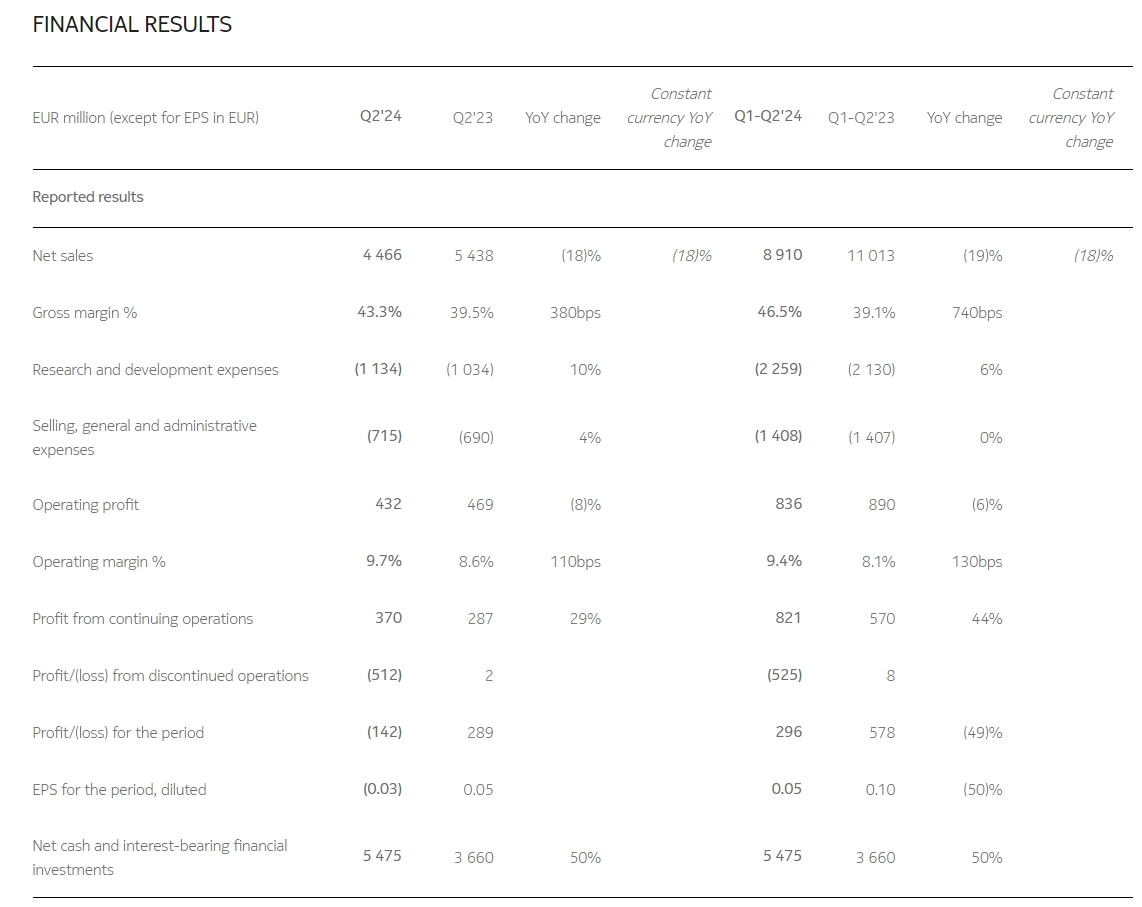

Q2 net sales declined 18% y-o-y in constant currency (-18% reported) primarily due to strong year-ago quarter in India.

Submarine Networks treated as discontinued operation.

Positively, order intake trends continued to improve, particularly in Network Infrastructure.

Comparable gross margin in Q2 increased by 450bps y-o-y to 44.7% (reported increased 380bps to 43.3%), mainly driven by Mobile Networks, in part benefiting from the resolution of an outstanding contract negotiation.

Q2 comparable operating margin decreased 190bps y-o-y to 9.5% (reported up 110bps to 9.7%), mainly due to low net sales coverage of operating expenses which more than offset the Mobile Networks contract resolution.

Q2 comparable diluted EPS of EUR 0.06; reported diluted EPS of negative EUR 0.03. Q2 reported EPS impacted by non-cash impairment charge of EUR 514 million related to Submarine Networks, presented as discontinued operation.

Q2 free cash flow of EUR 0.4bn, net cash balance EUR 5.5bn. Buyback program planned to be accelerated.

Significant progress with gross cost savings program, with EUR 400 million run-rate of savings already actioned.

Nokia's full year 2024 outlook is unchanged. Nokia currently expects comparable operating profit of between EUR 2.3 billion and 2.9 billion and free cash flow conversion from comparable operating profit of between 30% and 60%.

PEKKA LUNDMARK, PRESIDENT AND CEO, ON Q2 2024 RESULTS

I am pleased to confirm that the improving order intake momentum we’ve talked about for the past couple of quarters has continued in the second quarter across the group and most notably in Network Infrastructure. This trend means our backlog further expanded and we look forward to a meaningful improvement in net sales in the second half. Generally, the market remains uncertain, so we will continue to be agile and prudently manage our cost base as we navigate this environment.

In Q2, we announced two significant transactions in Network Infrastructure in support of our strategic pillar of actively managing our portfolio. On 27 June, we announced an agreement to sell our Submarine Networks business to the French State. We also announced our intention to acquire Infinera to increase the scale and profitability of our Optical Networks business. This will enable us to deliver faster innovation and expand our position both with webscale customers and regionally in North America. These transactions will focus and strengthen our Network Infrastructure business with its future built on three market-leading units in Fixed Networks, IP Networks and Optical Networks. We are investing in Network Infrastructure as we see a compelling opportunity in this business to drive mid-single digit net sales growth and improve our profitability to a mid-to-high teens operating margin over time.

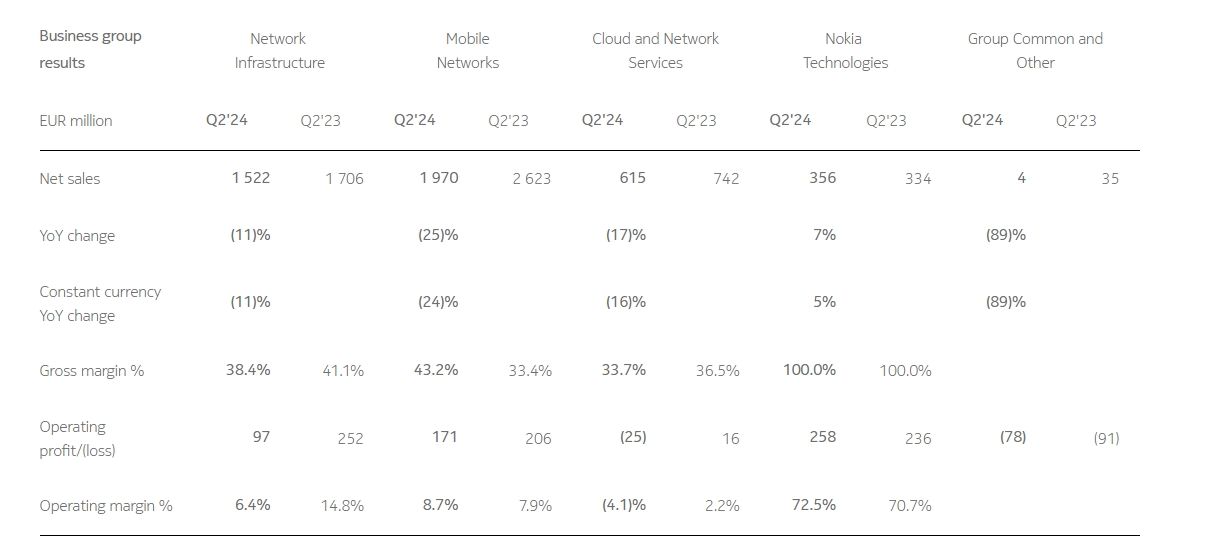

Our financial performance in the second quarter continued to be impacted by the ongoing market weakness with net sales declining 18% year-on-year in constant currency. The most significant impact was the challenging year-ago comparison period which saw the peak of India's rapid 5G deployment with India accounting for three quarters of the decline. In the quarter there was a benefit of EUR 150 million to both net sales and operating profit in Mobile Networks related to a portion of our contract resolution with AT&T. Our comparable operating margin was 9.5% compared to 11.4% in the prior year. We have made significant progress on our cost savings program and have already actioned run-rate savings of EUR 400 million out of our targeted EUR 800 million to EUR 1.2 billion gross cost savings by 2026.

Q2 was another strong quarter for cash generation with free cash flow of EUR 394 million as our working capital position continues to normalize. Our improving cash generation means the board now intends to accelerate our on-going EUR 600 million buyback program with the view to completing it by the end of this year, compared to the previous end of 2025 target.

In Network Infrastructure we secured a number of important design wins in the quarter. We won several important fiber deals, including in the US, and received orders from a US distributor for both Fixed and IP products as we gear up to supply operators under the BEAD program. It is also notable that we returned to growth in North America which was one of the first markets where we saw the 2023 market slowdown. With the challenges of 2023 behind us, and more normalized customer inventory levels, we believe we can now look forward to a stronger second half and a return to growth, which we expect to continue into 2025.

In Mobile Networks the market dynamic remains challenging as operators continue to be cautious. However there has been significant customer tendering activity and we have won a number of deals this year. This has included winning new customers such as MEO in Portugal, and increasing our footprint with existing customers, demonstrating the strength of our product offering. We also concluded negotiations with AT&T related to our existing RAN contracts. This gives us clarity on the path forward and ensures that we maintain the value agreed in the contracts.

In Cloud and Network Services we are making good progress with winning deals and with our organic efforts to bring new API capabilities and orchestration automation to customers. In Q2 we signed Network as Code collaboration agreements bringing our ecosystem total to 16, which includes new agreements with operators such as Orange, Telefónica, and Turkcell along with ecosystem players Google and Infobip.

In Nokia Technologies we signed an agreement with a video streaming platform covering the use of Nokia’s multimedia technology. This is an early step in what can be a meaningful opportunity for Nokia in the future.

Looking forward, we believe the industry is stabilizing and given the order intake seen in recent quarters we expect a significant acceleration in net sales growth in the second half. While the dynamic is improving, the net sales recovery is happening somewhat later than we previously expected, impacting our business group net sales assumptions for 2024. Despite this, we remain solidly on track to achieve our full year outlook supported by our quick action on cost. We are currently tracking towards the mid-point or slightly below the mid-point of our comparable operating profit guidance of EUR 2.3 to 2.9 billion and towards the higher-end of our free cash flow conversion guidance of 30% to 60%.